Key takeaways

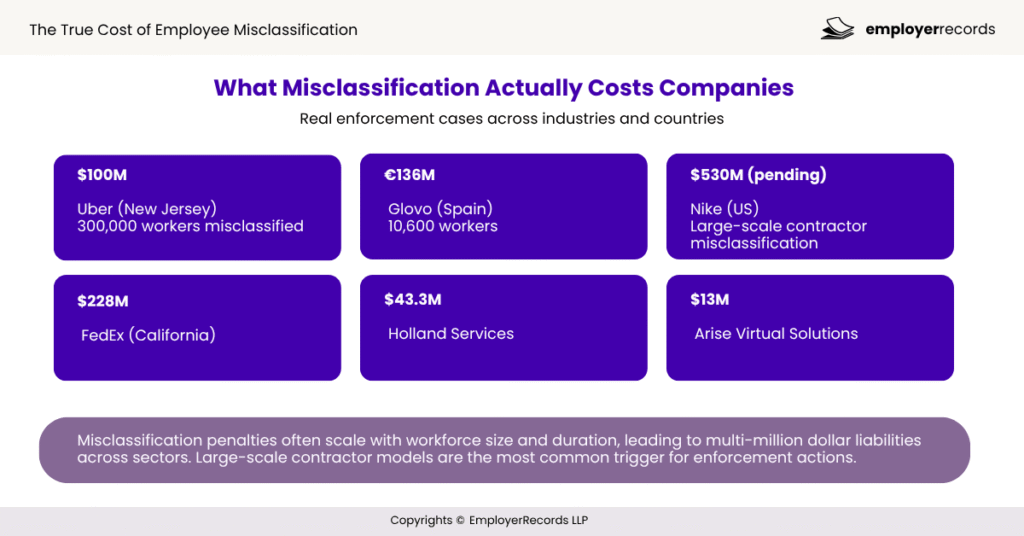

- Nike faces a potential $530 million tax bill. Uber paid $100 million in a single US state. Glovo was fined €136 million across two rulings in Spain. These are not edge cases, they are what happens when contractor arrangements are not legally sound.

- Misclassification exposes companies to back taxes, unpaid social contributions, statutory benefit repayments, civil fines, and in Germany, France, Spain, and Australia, criminal prosecution of individual directors.

- The contract label does not protect you. In Germany, France, Brazil, the Netherlands, and Australia, regulators look at how the working relationship actually operates, not what it says on paper.

- Lookback periods are long. The standard is 3 to 6 years across most markets. In Germany, intentional misclassification triggers a 30-year retroactive assessment under §25 SGB IV, with 12% annual interest.

- Enforcement is accelerating. The Netherlands lifted its moratorium on January 1, 2025. The EU Platform Work Directive takes effect in 2026. The US, UK, and Australia are using AI-assisted auditing to identify misclassification at scale.

- An Employer of Record eliminates misclassification risk entirely by making the EOR the legal employer of record in each country, transferring classification liability away from your company.

Nike is staring down a potential $530 million tax bill. Uber paid $100 million in a single US state. Glovo was fined €79 million in Spain, then €57 million again the following year.

None of these are freak outcomes. They are what happens when companies scale fast across borders, lean heavily on contractor arrangements, and assume the label on the contract is what the government will look at.

It isn’t.

In most countries, what matters is how the working relationship actually operates, not what it says on paper. Governments can go back years, sometimes decades, to collect what’s owed. Back taxes, unpaid social contributions, statutory benefits the worker should have received, interest on all of it, fines on top.

In Germany, executives go to prison personally. In Spain, entire platform business models have been challenged in court. In the Netherlands, a years-long enforcement moratorium ended on January 1, 2025, and companies that had been running borderline contractor arrangements are now scrambling to respond.

This article covers 30 countries. For each one: what test regulators use to decide whether someone should have been an employee, what the financial exposure looks like, how far back claims can go, and whether directors face criminal liability.

Where possible, we have linked directly to the source legislation, court decision, or government guidance, not to secondary commentary.

Before you read: The penalty figures here reflect maximum statutory fines and documented case settlements. Your actual exposure depends on how many workers were misclassified, for how long, and whether regulators consider the violation willful. Use this as a map, not a final answer. If you are making classification decisions, talk to a local employment lawyer.

The True Cost of Employee Misclassification

Global enforcement is rising · Penalties stack · Lookback periods are long

Back taxes · Social contributions · Employee benefits · Interest · Civil fines · Criminal liability

Typical lookback

- 3–6 years standard

- Germany: up to 30 years

- Fraud cases: unlimited (US)

Penalty exposure

- Per-worker fines apply

- Interest accumulates annually

- No cap in some countries (Brazil)

Real-world cases

- $100M → Uber (New Jersey)

- €136M → Glovo (Spain)

- $530M → Nike (pending)

Misclassification penalties often include back taxes, benefits, and fines accumulated over several years, making total exposure significantly higher than expected.

Why the contract label is not your defence

If your company pays someone as an independent contractor, but that person works full-time hours on your tasks, follows your instructions, uses your equipment, and could not realistically offer those same services to anyone else, most countries will say you have an employee. What the contract calls them is irrelevant.

Governments care about this for two reasons. Workers miss out on protections they are legally entitled to: sick pay, holiday pay, pension contributions, overtime, redundancy rights.

And governments lose payroll tax revenue. The U.S. Department of Labor estimates the United States alone loses $3 to $4 billion a year from misclassification. (DOL Wage and Hour Division)

When regulators confirm misclassification, the consequences stack in layers:

- Back taxes the employer should have been withholding, plus interest

- The employer’s full share of social contributions (pension, health insurance, unemployment) for the entire period

- Back payment of every employment benefit the worker was denied, including leave, overtime, and pension top-ups

- Civil fines from the relevant labour or tax authority

- In many countries, personal criminal liability for directors and executives

One more thing that catches global companies off guard: a worker can be a contractor under one country’s law and an employee under another’s, simultaneously.

Someone hired as a contractor for a UK client, working from Germany, could be classified as an employee under German law even while the UK arrangement is technically fine. You need a country-by-country view. A single global template is not a classification strategy.

What the real cases look like

Uber, New Jersey, United States: $100 million (2022) Uber and its subsidiary Rasier LLC misclassified approximately 300,000 drivers as independent contractors. New Jersey’s Department of Labor assessed $100 million in unpaid state payroll taxes and penalties. Uber has faced similar enforcement in California, Massachusetts, and the UK. (NJ Department of Labor)

Glovo, Spain: €136 million across two rulings (2022 and 2023) Spain’s Labor Inspectorate fined Glovo €79 million in 2022 for misclassifying over 10,600 riders, then nearly €57 million again in 2023. Spain’s Rider Law, the Ley Rider (Real Decreto-ley 9/2021), presumes platform delivery workers are employees unless the platform proves otherwise. The burden of proof sits with the company, not the worker. Glovo is appealing. The rulings stand as the largest misclassification penalties in European history.

Nike, United States: up to $530 million (pending) Nike faces potential tax fines exceeding $530 million for allegedly misclassifying thousands of temporary office workers as contractors. The case has not concluded. It is among the largest pending misclassification exposures cited in IRS proceedings. (Reported by Reuters, citing IRS records.)

UK Research and Innovation, United Kingdom: £36 million A public sector research body, not a tech platform, paid £36 million after a finding that it had denied employee protections to workers. This case is cited often because it removes the assumption that misclassification is a private sector or gig economy problem.

FedEx, California, United States: $228 million (2015) FedEx settled a class-action lawsuit for $228 million after more than 2,000 drivers in California were found to have been incorrectly classified as independent contractors. One of the largest misclassification settlements in US legal history.

Holland Services, United States: $43.3 million (2021) A DOL Wage and Hour Division investigation found Holland Services had misclassified 700 workers. The company owed nearly $43.3 million in back wages and damages. (DOL enforcement database)

Arise Virtual Solutions, United States: $13 million (2022) Arise agreed to pay over $13 million, including $3 million in back wages to more than 22,000 customer service agents, to settle misclassification claims covering workers classified as contractors running their own small franchises.

The pattern: In every one of these cases, the contractor model was a deliberate business decision, not an accident. Regulators know this. “We didn’t realise” is a weak defence in most jurisdictions. Willful misclassification carries higher fines and, in several countries, criminal prosecution.

Country-by-Country Reference Table

Risk levels reflect a combination of penalty ceiling, enforcement activity, and criminal exposure for directors. The table is a starting point. Legal advice in each jurisdiction is irreplaceable.

The table below covers 31 countries. It is a starting point, not a substitute for legal advice. Risk levels reflect a combination of penalty ceiling, enforcement activity, and criminal exposure for directors.

| Country | Classification Test | Max Financial Exposure | Back Pay Lookback | Criminal Liability? | Risk |

| 🌎 AMERICAS | |||||

| 🇺🇸 United States | IRS 20-factor test + FLSA ‘economic realities’ test (revised Jan 2024) | Back FICA taxes (20–100% of owed amount); $50/unfiled W-2; CA state adds up to $25,000/worker; criminal fines up to $1,000/worker | 3 yrs (IRS standard); no limit for fraud | Yes, up to $1,000/worker fine + prison for willful violations | Very High |

| 🇨🇦 Canada | CRA 4-factor test: control, tools, profit/loss risk, integration | Back CPF/EI contributions + interest; administrative monetary penalties from CAD $3,000/violation | 3–7 years | Yes, for willful tax evasion | High |

| 🇧🇷 Brazil | CLT habitual service + subordination test (economic dependence matters) | Full back wages + FGTS (Fundo de Garantia) contributions + 40% FGTS penalty on severance; no statutory cap | 5 years | Yes, serial violators face criminal charges | Very High |

| 🇲🇽 Mexico | IMSS subordination test + 2021 outsourcing reform (near-ban on contractor use) | MXN 108.57/day per misclassified worker + full statutory benefit back-payment | 5 years | Yes, tax fraud provisions apply | High |

| 🇦🇷 Argentina | AFIP economic dependence + regularity of service test | 30% surcharge on unpaid contributions + full back pay; no capped maximum | 5 years | Yes | High |

| 🇨🇴 Colombia | Ministry of Labor: integration + habitual service test | Up to 5,000x monthly minimum wage per violation + unpaid benefit repayment | 3 years | No (civil only) | Medium |

| 🌍 EUROPE | |||||

| 🇬🇧 United Kingdom | IR35: mutuality of obligation + control + substitution right (hiring company determines status since Apr 2021) | Unlimited for willful; HMRC recovers PAYE + employer NI from deemed employer; holiday pay claims run up to 6 years under Agnew ruling (UKSC 2023) | 6 years (holiday pay); 4 years (PAYE) | Yes, up to 2 years prison under National Minimum Wage Act | Very High |

| 🇩🇪 Germany | Deutsche Rentenversicherung: integration + economic dependence; 83% single-client income rule triggers mandatory pension contributions | Back social security contributions + employer and employee portions; up to 4 yrs (standard) or 30 yrs (intentional) per §25 SGB IV; €10M for intentional tax evasion; 12%/yr interest | 4 yrs standard; 30 yrs intentional | Yes, up to 5 yrs prison for managing directors (§266a StGB) | Very High |

| 🇫🇷 France | Travail dissimulé: Labour Inspectorate assesses control + integration + economic dependence | €15,750/worker + 3 yrs back URSSAF social contributions; criminal: €45,000 fine + 3 yrs prison | 3 years | Yes, 3 yrs prison + €45,000 | Very High |

| 🇪🇸 Spain | Labour Inspectorate integration test; Ley Rider (2021) presumes employment for platform workers | Up to €187,515 per serious infraction; Glovo paid €79M + €57M; ongoing enforcement through 2027 under ITSS strategic plan | 4 years | Yes, for systematic violations | Very High |

| 🇳🇱 Netherlands | Wet DBA (2016): substance over form; enforcement moratorium lifted Jan 2025; Belastingdienst assesses control + integration + economic dependence | Retroactive payroll tax up to 5 years; fines in millions for confirmed cases; both client and contractor can be penalised | 5 years | Yes, directors face personal liability | Very High |

| 🇮🇹 Italy | INPS: subordination + integration + personal service test | Unpaid INPS contributions + 30% surcharge; fines up to €50,000; automatic reclassification | 5 years | Yes, criminal fines for willful evasion | High |

| 🇸🇪 Sweden | Skatteverket economic reality test: who bears financial risk? | Back taxes + 25% surcharge; pension deficits must be repaid in full | 5 years | Yes, tax evasion provisions | High |

| 🇧🇪 Belgium | ONSS 9-criteria test: authority, financial risk, integration | Back ONSS contributions + up to 80% surcharge; solidarity contribution also applies | 5 years | Yes, for willful misclassification | High |

| 🇵🇱 Poland | ZUS economic dependence test; EU Platform Work Directive implementation 2026 | Back ZUS social contributions + administrative fines | 5 years | Yes | Medium |

| 🇮🇪 Ireland | Revenue Commissioners: code of practice on employment vs self-employment (12 factors) | Back PRSI + income tax + USC + interest; Revenue audit triggered across full workforce | 4 years | No (civil only) | Medium |

| 🇵🇹 Portugal | ACT: subordination + exclusivity + dependency test | Back social security + fines up to €9,600/worker; automatic reclassification | 5 years | No (civil only) | Medium |

| 🌏 ASIA-PACIFIC | |||||

| 🇦🇺 Australia | Fair Work Act: totality of relationship test (amended Aug 2024 to overturn High Court’s contract-only focus); sham contracting threshold lowered to ‘reasonable belief’ | AUD $469,500/contravention (company); AUD $4.695M for ‘serious contravention’; directors personally liable separately; back super guarantee + leave | 6 years | Yes, directors personally liable; wage theft criminal in VIC and QLD | Very High |

| 🇯🇵 Japan | Labour Standards Act: control test + continuity of relationship; enforcement increasing since 2024 | Unpaid social insurance + labour standards penalties; increased audit activity from 2024 | 2–5 years | Limited, civil penalties dominant | Medium |

| 🇸🇬 Singapore | MOM Employment Act: substance-over-form; CPF Board assesses financial control + integration | SGD $10,000/worker + back CPF contributions (employer + employee portions) | Up to 5 years | Yes, SGD $10,000 fine or 6 months jail | High |

| 🇮🇳 India | Labour Codes (2020, now being implemented): PF/ESI registration triggers; SS Code §38 governs enforcement | INR 100,000 fine + INR 30,000/day for continuing violations (SS Code); plus back PF/ESI contributions | 3 years | Yes, up to 3 yrs imprisonment (SS Code §72) | High |

| 🇵🇭 Philippines | DOLE: regularization presumption after 6 months; ‘labor-only contracting’ ban | Back SSS, PhilHealth, Pag-IBIG contributions + regularization order; reinstatement with full back pay | 3 years | Yes | Medium |

| 🇮🇩 Indonesia | Manpower Law No.13/2003: outsourcing restrictions; only limited roles permitted for contractors | Automatic employee status + full benefit back-payment + fines | 2 years | Yes | Medium |

| 🇰🇷 South Korea | Labour Standards Act: 4-criteria test (instruction, integration, schedule, tools); enforcement ramping since 2023 | Back pay + National Pension + health insurance contributions + fines | 3 years | Yes | Medium |

| 🇳🇿 New Zealand | Employment Court economic reality test: 6 factors under Employment Relations Act 2000 | NZD $50,000/individual + back Holidays Act entitlements + KiwiSaver contributions; 6-year look back on holiday pay | 6 years | Yes, directors personally liable | High |

| 🌐 MIDDLE EAST, AFRICA & OTHERS | |||||

| 🇦🇪 UAE | MOHRE: work permit compliance + labour contract registration; Federal Decree Law No.9/2024 increased fines effective Aug 31 2024 | AED 100,000 to AED 1,000,000 per violation under new Decree Law 9/2024; doubling for repeat violations within 3 yrs | N/A — at-will regulatory enforcement | Yes, imprisonment up to 6 months + possible deportation of worker | High |

| 🇸🇦 Saudi Arabia | GOSI registration + Nitaqat Saudization compliance | SAR 10,000/worker + suspension from government contracts | 3 years | Yes | Medium |

| 🇿🇦 South Africa | Labour Relations Act s.198A deeming provision (presumption of employment for low-earning workers) | Automatic deemed employee status + full back pay order by CCMA | 3 years | No (civil only) | Medium |

| 🇨🇳 China | Labour Contract Law: mandatory written contracts + automatic employment after 1 month without contract | Back social insurance + 2x monthly salary/year without written contract; automatic employment relationship created | 2 years | Yes, for serious violations | High |

| 🇹🇷 Turkey | Labour Law No.4857: integration + continuity + subordination | Back SGK contributions + fines up to TRY 100,000; reclassification order | 5 years | Yes | Medium |

The countries where getting this wrong is most expensive

Germany: where a single contractor can cost you 30 years of back taxes

Germany calls it Scheinselbständigkeit, or fake self-employment. The German Pension Insurance (Deutsche Rentenversicherung, DRV) is the primary enforcement body, and it operates aggressively.

In 2023 alone, around 42,000 cases of suspected fake self-employment were investigated, resulting in €487 million in retroactive contributions. (Source: DRV enforcement reporting, cited in Jobbers.io analysis of DRV 2024 data.)

The 30-year lookback is real and has a specific legal basis. Under §25 SGB IV, standard misclassification triggers a 4-year retroactive assessment of social security contributions. If the misclassification is found to be intentional, that window extends to 30 years, with 12% annual interest on everything owed. For a long-running contractor relationship, this can destroy a company financially.

The 83% income rule deserves particular attention. If a freelancer earns 83% or more of their total income from a single client, German law treats them as economically dependent.

That triggers mandatory pension insurance contributions regardless of their formal contractor status. Many companies encounter this rule for the first time when the DRV contacts them. (Source: §2 SGB VI; §12a TVG)

Under §28e(1) SGB IV, when misclassification is confirmed, the hiring company owes both the employer and the employee portions of social security, not just the employer’s share.

It cannot deduct the employee portion from their pay except for the last three months. The fees already paid to the contractor are treated as net wages, then “grossed up” to calculate a notional gross salary, which substantially inflates the base for the social security calculation. (Source: Schlun & Elseven Rechtsanwälte)

The criminal exposure sits in §266a StGB. Managing directors who knowingly withhold employee social security contributions face up to 5 years in prison, personally, not the company. In 2024, the German Customs Authority (Hauptzollamt) conducted nationwide raids across several industries targeting suspected Scheinselbständigkeit. (Source: Hogan Lovells)

What typically triggers an investigation: the worker leaves and files for unemployment benefits. The Bundesagentur für Arbeit refers the case to the DRV. By the time the investigation reaches the company, the retroactive window is already accumulating interest.

Spain: gig workers are presumed employees by law

Spain’s Ley Rider (Real Decreto-ley 9/2021) came into force in August 2021. It created a legal presumption that platform delivery workers, couriers, food delivery riders, anyone doing last-mile delivery via a digital algorithm, are employees. The burden of proof sits with the platform, not the worker. Platforms must prove contractor status, not the other way around.

Glovo’s experience is the most documented example. The Labour Inspectorate (Inspección de Trabajo y Seguridad Social, ITSS) concluded that Glovo’s riders were employees. First fine: €79 million in 2022. Second fine: nearly €57 million in 2023.

Combined total across two rulings: over €136 million for roughly 10,600 workers. Glovo is appealing. The ITSS published a strategic enforcement plan covering 2025 to 2027 that specifically names platform economy enforcement as a priority. (Source: Spanish Ministry of Labour)

The maximum per-infraction fine under the Ley de Infracciones y Sanciones en el Orden Social (LISOS) is €187,515 for serious violations. When misclassification covers thousands of workers, the total multiplies accordingly. The social contribution lookback is 4 years.

Netherlands: enforcement started January 1, 2025

The Netherlands has been working on this since 2016, when the Wet DBA (Wet Deregulering Beoordeling Arbeidsrelaties) replaced the old VAR system for freelancers.

The law was designed to clarify when a contractor is legally an employee, what Dutch law calls schijnzelfstandigheid, or false self-employment. Enforcement was placed on hold almost immediately while the government refined the implementation framework. That moratorium ended on January 1, 2025.

From that date, the Dutch Tax Authority (Belastingdienst) can audit and impose retroactive payroll tax assessments going back up to 5 years.

Fines run into the millions for confirmed cases. Both the hiring company and the contractor can be penalised, which creates a two-sided incentive to get the classification right.

The Belastingdienst said it would focus on severe and systematic cases in the first year of enforcement, but companies are not waiting to find out the threshold and are reclassifying contractors proactively. (Source: Belastingdienst; Atlas HXM)

The factors the Belastingdienst examines: Does the worker control their own schedule and methods? Do they work for multiple clients? Do they bear genuine financial risk? Do they use their own tools? The more of these that point toward “no,” the higher the reclassification risk.

The Ministry has published a working relationship assessment tool (webmodule arbeidsrelatie) to help companies self-evaluate before an audit.

United Kingdom: IR35, holiday pay lookbacks, and six years of exposure

The UK’s IR35 rules date to 2000, but the enforcement landscape shifted materially in April 2021. From that date, medium and large private-sector businesses became responsible for determining whether their contractors should be classed as employees for tax purposes, not the contractors themselves.

If the determination is wrong, HMRC pursues the hiring business for unpaid PAYE and employer National Insurance.

HMRC cross-references self-assessment returns, company records, and contract details. Compliance checks typically take 18 to 21 months from initiation to settlement.

The offset rules changed in April 2024, meaning HMRC now credits tax already paid by the contractor against the employer’s liability, which reduced the double-taxation issue that existed previously. (Source: HMRC guidance)

The holiday pay exposure is frequently underestimated. The UK Supreme Court’s October 2023 ruling in Chief Constable of the Police Service of Northern Ireland v Agnew [UKSC 33] confirmed that where workers have been systematically underpaid holiday pay, the claim can cover the entire series of deductions going back years, not just the previous 3-month window.

For a worker misclassified across a 6-year period, the full 6 years of underpaid holiday is claimable in one action. (Source: Labour Relations Agency)

The DWP IR35 case, which ran from 2017 to 2024, resulted in HMRC raising an £87.9 million tax bill against the Department for Work and Pensions for incorrectly determining contractor status across its off-payroll workforce. Public sector or private sector, the exposure mechanism is the same.

Australia: the law changed in 2024 and the fines went up fivefold

Australia’s High Court ruled in February 2022 in CFMMEU v Personnel Contracting Pty Ltd [2022] HCA 1 that whether someone is an employee or contractor should be determined by the written contract terms, not the practical reality of how the work was performed. (Source: Wikipedia case summary)

The government then changed the law. The Fair Work Legislation Amendment (Closing Loopholes) Act 2024, which received royal assent on 26 February 2024, reverted to the “totality of the relationship” test, looking at real working practices rather than just what the contract says.

It also lowered the sham contracting offence threshold from recklessness to “reasonable belief,” making it easier for regulators to establish a violation. (Source: Baker McKenzie Resource Hub)

The penalty increases are substantial. Under the amended Fair Work Act, the maximum penalty for a “serious contravention” is now AUD $4.695 million per company, up from AUD $939,000.

A standard contravention where the company “reasonably should have known” the worker was misclassified costs up to AUD $469,500. Directors are personally liable on top of these company fines. Add back superannuation guarantee, six years of back leave entitlements, and in Victoria and Queensland, wage theft laws that carry criminal prosecution. (Source: National Law Review)

Brazil: the highest back-pay exposure of any major market

Brazil’s Consolidation of Labour Laws (CLT, Consolidação das Leis do Trabalho) dates to 1943 and has been continuously updated to close contractor loopholes. Courts apply four criteria: subordination, regularity of service, personal performance, and payment for service. Where those are present, the worker is an employee regardless of any contract saying otherwise.

The FGTS (Fundo de Garantia do Tempo de Serviço) is what makes Brazil’s exposure so large. Every employer must contribute 8% of monthly salary to this government-managed severance fund for each employee.

If a contractor is reclassified, the company owes all unpaid FGTS contributions across the full period, a 40% penalty on that FGTS balance as a termination charge, plus 13th month salary, vacation pay, overtime, and all other statutory entitlements.

The five-year lookback means this accumulates quickly for long-running relationships.

Brazil’s 2017 Labour Reform (Lei 13.467) was intended to make contracting more accessible, but courts have applied it inconsistently, and parts were revised almost immediately.

The practical position remains: if someone works regular hours for you, follows your direction, and works exclusively for you, Brazilian labour courts will almost certainly call them an employee regardless of the contract structure.

There is no cap on back-pay liability in Brazil. The total is determined by number of workers, duration, and salary level. Major multinationals have faced eight-figure claims from Brazilian labour tribunals.

Five things companies consistently get wrong

Most misclassification findings come from ordinary business practices that companies have run unchallenged for years. Here is what regulators actually focus on.

1. Treating duration as a non-issue

A 3-month project-based contractor engagement is fundamentally different from someone who has worked full-time for your company for 3 years. Duration does not create an employment relationship by itself, but it is a serious red flag in every jurisdiction.

In Germany, the DRV targets long-running single-client relationships specifically. In Brazil and the Netherlands, extended duration alongside any other employment indicator is very difficult to defend. Most employment lawyers recommend reviewing any contractor relationship that has passed the 12-month mark.

2. The single-client concentration problem

In Germany the law is explicit: a contractor earning more than 83% of their income from one client owes mandatory pension contributions regardless of their classification.

In France, Brazil, and the Netherlands, financial dependence on a single company is one of the strongest indicators of an employment relationship. Companies running preferred-supplier or embedded contractor arrangements, where the person works with them and no one else, are building exactly this problem.

3. Operational integration

If a person attends your internal team meetings, appears on your org chart, carries a company email address, uses company equipment, follows company procedures, and their colleagues do not know they are a contractor, they are integrated into your business.

Regulators look at the substance of the relationship. A contractor who operates like a full-time employee in every practical sense will be classified as one. This is especially relevant in Australia after the 2024 amendments, in Spain under the Rider Law, and in the UK under HMRC’s working practices assessment framework.

4. Using one contract template globally

A contractor agreement that holds up in the United States may be unenforceable in Germany, void in Brazil, and ignored entirely in France.

Each country has its own classification test, and many of them, including Germany, Brazil, France, and the Netherlands, explicitly state that the contract label is not determinative. What matters is how the relationship works in practice. A single global template is not a compliance approach.

5. No audit before fundraising or acquisition

Investors and acquirers run misclassification checks as a standard part of due diligence, particularly in tech and platform businesses.

If your company has grown through a contractor-heavy model and those contractors are misclassified, you will either lose the deal or take a valuation reduction to cover the contingent liability. The right time to identify and fix misclassification is before you are under due diligence pressure, not during it.

The costs that never appear in the government notice

The penalty in the initial enforcement notice is only part of what a misclassification finding actually costs. Companies that go through these investigations also typically face:

- A full workforce audit. Once regulators identify misclassification in one area, they audit the whole workforce picture. The original finding is rarely the last.

- Reclassification orders. All affected workers must be reclassified retroactively, with every statutory entitlement back-paid from the deemed start date of employment.

- Stop-work orders. In 2022, the U.S. Department of Labor issued stop-work orders to five out-of-state contractors in New Jersey for misclassifying construction workers. The work stopped completely while the matter was resolved.

- Intellectual property disputes. In Germany, Canada, and India, IP created during a working relationship may legally belong to the worker if they were not formally employed. A contractor who built core software may own it.

- Investor and lender complications. Contingent misclassification liabilities are material disclosures in fundraising rounds and debt financing. Some founders have been required to personally escrow funds against outstanding claims before transaction closings could proceed.

- Talent exits. Converting misclassified workers to employment status changes their working conditions, their cost structure, and in some cases their willingness to stay. Contractors who specifically chose freelance status sometimes leave rather than convert, taking institutional knowledge with them.

The maths on contractor “savings”: U.S. companies save roughly $3,710 per worker per year by engaging them as contractors instead of employees. (Source: Tarmack.com analysis.) For 50 contractors over 3 years, that is around $557,000 in avoided costs. If those workers are misclassified and a DOL or IRS investigation covers that period, the total exposure in back taxes, contributions, fines, legal costs, and penalties can exceed $5 million. The savings model only works if the classification is correct.

What is changing in enforcement right now

The EU Platform Work Directive

The Directive was formally adopted by the European Parliament in 2024 and must be implemented by EU member states by 2026.

It creates a legal presumption of employment for platform workers across all EU countries, covering Spain, Germany, France, Italy, the Netherlands, Belgium, Poland, and the rest. Platforms that want to engage workers as contractors will need to actively rebut this presumption on a case-by-case basis.

Countries that already have strict frameworks, particularly Spain, France, and Germany, are expected to implement the most aggressively. (Source: European Commission)

Netherlands DBA enforcement (active since January 2025)

This is not a future development. The moratorium that had been in place since 2016 ended. The Belastingdienst is auditing now, and retroactive assessments covering 2020 to 2025 are possible for companies that ran undocumented or structurally weak contractor arrangements during the moratorium period.

Data-driven auditing in the US, UK, and Australia

The U.S. DOL and IRS have both documented using data matching and algorithmic pattern recognition to identify potential misclassification at scale, cross-referencing 1099 filings, payroll records, and industry benchmarks. HMRC has invested in compliance technology targeting off-payroll workers.

The Australian Tax Office applies similar methods to superannuation guarantee non-compliance. The era of relying on slow enforcement to avoid detection is ending.

How to reduce the risk without stopping contractor use

None of this requires abandoning contractor arrangements. It requires doing them correctly.

Assess classification country by country, not by template

Germany looks at economic dependence and single-client income concentration. France looks at subordination and concealed employment.

Australia looks at the totality of the working relationship. Ireland applies a 12-factor code of practice. One contract template cannot satisfy all of these. For any market where you have significant contractor headcount, commission a local employment law assessment.

Document independence with specifics, not platitudes

The strongest defence against a misclassification finding is evidence that the contractor genuinely operates independently: multiple clients, their own tools and professional insurance, their own registered business entity, real flexibility over how and when they deliver the work.

An annual letter stating “you are an independent contractor” is not evidence of independence. Records of their other clients, their own business expenses, and their contractual right to substitute someone else to perform the work are.

Review long-running relationships every year

Any contractor relationship that has passed 12 months should be formally reviewed. The question is not “do we have a contract that says contractor?” The question is “if a regulator looked at this relationship today, what would they conclude?” If the honest answer is “they might call it employment,” adjust the arrangement or convert to employment. Waiting costs more.

Audit before significant corporate events

Before a funding round, an acquisition process, or entry into a new market, audit your contractor arrangements. It is far cheaper to find and remediate problems before investors or regulators do it for you. Disclosing a material contingent liability in a data room is considerably more painful than fixing the classification beforehand.

Consider an Employer of Record in high-risk markets

In Germany, Brazil, the Netherlands, Spain, and Australia, the risk of getting classification wrong is high and the penalties are severe. An Employer of Record (EOR) legally employs the worker in the relevant country, handling the employment contract, payroll, tax withholding, and all statutory benefits.

Because the EOR is the legal employer, the misclassification risk sits with them rather than with your company. This is not the right solution for every situation. For genuinely project-based work with a true independent contractor who has multiple clients and bears real financial risk, a proper contractor agreement works fine.

For recurring, integrated, long-term work in high-risk jurisdictions, EOR is frequently the cleaner and more defensible path.

See our related guide: How EORs Prevent Employee Misclassification

Sources and further reading

- U.S. DOL Wage and Hour Division: dol.gov/agencies/whd

- DOL Final Rule on Employee/Contractor Classification (January 2024): federalregister.gov

- Germany §25 SGB IV (retroactive social security limit): gesetze-im-internet.de

- Germany §28e(1) SGB IV (employer liability for contributions): gesetze-im-internet.de

- Germany §266a StGB (criminal liability for non-payment): gesetze-im-internet.de

- Germany misclassification legal analysis, Schlun & Elseven: se-legal.de

- Germany enforcement activity, Hogan Lovells: hoganlovells.com

- Spain Ley Rider (Real Decreto-ley 9/2021): boe.es

- Spain ITSS and Ministry of Labour: mites.gob.es

- Netherlands Belastingdienst: belastingdienst.nl

- Netherlands DBA enforcement 2025, Atlas HXM: atlashxm.com

- UK HMRC IR35 off-payroll working: gov.uk

- UK HMRC PAYE liability in off-payroll cases: gov.uk

- UK Supreme Court, Chief Constable v Agnew [UKSC 33] (2023): lra.org.uk

- Australia CFMMEU v Personnel Contracting [2022] HCA 1: en.wikipedia.org

- Australia Fair Work Legislation Amendment (Closing Loopholes) Act 2024: legislation.gov.au

- Australia Baker McKenzie misclassification risk analysis: resourcehub.bakermckenzie.com

- Brazil CLT (Decreto-Lei No. 5.452/1943): planalto.gov.br

- India Labour Code penalties, India Briefing: india-briefing.com

- UAE Federal Decree Law No.9/2024, DLA Piper: knowledge.dlapiper.com

- UAE Federal Decree Law No.9/2024, Clyde & Co: clydeco.com

- Global misclassification risk analysis, Clyde & Co (October 2024): clydeco.com

- Baker McKenzie global misclassification risk map: resourcehub.bakermckenzie.com

- EU Platform Work Directive, European Commission: ec.europa.eu

This article is published by EmployerRecords.com for research purposes only. It is not legal advice. Employment classification law changes frequently, varies significantly between jurisdictions, and must be applied to specific facts. Penalty figures reflect statutory maximums and documented case outcomes. Your actual exposure depends on your situation. Before making any classification decision, speak to a qualified employment lawyer in the relevant jurisdiction.